As many of us prepare to move our strategy courses online, we need video “shorts” that introduce core strategy principles to go along with key readings. By now, you may have already seen collections by David Kryscynski, Shad Morris, and others in the toolbox. Melissa Schilling has graciously made a new set of videos available that address core strategy principles not found in the other collections. See also her related collection focused around innovation strategy (note that there is some overlap). Below is her video introducing agency problems as a sample.

In addition, she covers the following topics that may be useful for a strategy course:

Print the Legend (2014) is a documentary about the 3-D printing industry, that offers an engaging case study covering industry, firm & technology life cycles, disruptive technologies, and strategy in emerging firms & industries. This industry was established in the 1980s focusing on large expensive printers for industrial use – Two key players dominated using different technologies. The market was seriously shaken by startups in the 2010s that drastically reduced pricing created a consumer market. As such, we see two distinct market segments (industrial & consumer) and two technologies (stereolithography & fused-deposition) all battling it out.

The film follows two startups from emergence through VC funding, and shows their diverging paths as one is acquired and one remains independent. MakerBot, hires an experienced Strategy Director who (with the VC) radically shifts the founding strategy. This leads to high turnover and eventually, founder exit and acquisition by a leading industrial 3-D printing incumbent. In contrast, FormLabs, takes a more emergent approach to strategizing and positioning. The award-winning film is very well-made and fun to watch – Students love it and learn from it. It features a prominent VC (Brad Feld) and startups that students may be aware of.

Teaching notes: The film (available on Netflix) runs 100 minutes, so with discussion, it takes a full 3-hour class. It is helpful toward the end of the semester as a “movie day” with popcorn and snacks – students appreciate a break the week before their big final project is due. It is helpful to spend about 20 minutes at the start of class giving a mini-lecture on firm & industry life cycles and disruptive technologies, to set up the film, as well as about 10 minutes at the end for a debrief. One can show the film in 10-20 minute segments, pausing to discuss what has happened so far. This case has been a big hit over the 2 years it has been in use. It’s a little logistically complex, and requires strict adherence to a schedule, but once you have it down, it’s a very easy class and case to teach. Full teaching notes, assigned pre-reading, slides, and film segments are available on Gina’s shared teaching site.

It’s been a red letter week in terms of the business combination scavenger hunt. In addition to Dyson entering electric cars, now we see Aston Martin going into the submarine business. These are both serious ventures. Dyson has had 400 staff members working on this project for over two years and expects to bring a product to market in 2020. One can’t resist wondering if it will really suck (I know, vacuum humor isn’t in vogue — if it ever was)…

More seriously, Dyson is a private company and so won’t face as much market pressure to explain why/how the business portfolio creates value. Also, while most of us are more familiar with their vacuum business, they are a diversified manufacturing company. This includes supplying inputs for the automobile industry among others. One might argue that they have more complementary assets to produce electric cars than Tesla had when they first started. But still…

Aston Martin’s effort is also serious. It’s worth noting that, unlike Dyson, they plan to do this with a partner, Triton Submarines, that is already a player in the luxury submarine market.

Drawing on the Strategy Diamond framework, a vehicle is the mode used to acquire resources needed to enter a new market. In this context, why would Dyson use organic growth to enter electric cars while Aston Martin forms a strategic alliance to enter submarines? In each case, the firm lacks important resources needed to enter. One might apply Capron & Mitchell’s Resource Pathway’s Framework. This could lead one to conclude that Dyson is overestimating the relevance of its internal resources (to go without a partner). In the case of Aston Martin, since their partner has all the capabilities needed to produce the product, the main asset that Aston Martin brings is their brand. This may be useful to court customers who are James Bond fans — Perhaps not the largest market segment among those seeking submarines.

Meanwhile, Ikea just acquired TaskRabbit — presumably a bid to vertically integrate into assembling the furniture they sell in kits.

These efforts do not necessarily restore one’s confidence in managers’ abilities to make reasoned decisions about the scope of the firm.

Shareholder activism is often identified as a mechanism to discipline managers and keep them focused on value creation for investors. An NPR story reports that shareholders in a zoo near Shanghai, frustrated that they weren’t making a profit on their investment, fed a live donkey to zoo tigers as a form of protest. At a shareholders meeting they voted in favor of feeding the donkey to the tigers to express their anger. Their objections center on the zoo’s debts and legal troubles. For two years, the investors said the venture has not been profitable. The video of the event has stoked public outrage and condemnation. While this is a rather unusual example of shareholder activism, it may spur some fruitful discussion in class. One of the interesting elements of this action is that the Corporate Social Responsibility literature would lead us to expect that investors have idiosyncratic preferences and will make trade-offs on returns (see this article by Mackey, Mackey & Barney). For example, one might expect that investors in a zoo would be willing to trade off financial returns to care for animals. A protest of poor profitability that hurts an animal seems especially unlikely. Yet there is is. As the cartoon implies, there are other ways for investors to protest…

Why isn’t the BCG matrix dead as a framework? I still consistently find that my students have been exposed to it (generally in Marketing). They don’t even understand that it is a framework for internal capital markets (where firms add value by serving as a source of funding) or that it is hopelessly flawed. It’s a dog, divest right away. If the sale generates cash, funnel it to any other management framework (even SWOT) and I’m sure it will create value.

Internal capital markets only create value when they perform better than external capital markets. Generally, this is because the parent company has better information than external markets about the business. I often describe how Big Pharma companies fund biotech startups — their inside knowledge of the science and downstream capabilities help them understand the potential. As such, their expertise and private information allows them to invest much more efficiently than external capital markets.

Gautam Ahuja won the 2016 BPS Irwin Outstanding Educator award. It became clear from student testimonials that the capstone ethics lecture was not just memorable, it was an emotional peak that few students (or teachers) ever reach. What follows is a brief description/outline of the lecture. While it certainly won’t do it justice, it may offer some important ideas for instructors to explore.

I have them debate an actual decision (that varies from year to year). Essentially, I pick some current significant and controversial business decision or event that is legal and ideally, morally ambiguous, or even amoral (not immoral), at least apriori, and then foster a discussion on its pros and cons. This reveals much deeper fundamental issues. To illustrate I have used the following in different years:

The decision by banks to award bonuses to traders for being on the “correct” side of the financial crisis deals in the years following the Lehman collapse

The decision by a chemical company to use local safety standards in its different markets, which is completely legal,

The decision to sell skin whitening creams in countries in India by large multinational companies,

Provision of significantly discounted or couponed milk products for newborns,

The federal reserves decision to keep interest rates low for the last x years and so on…

I then try and get them to debate this and, almost invariably, there emerge two sides to the issue. However what is interesting is that three other factors usually emerge: A) the problem is much deeper and more morally ambiguous than you thought, B) reflexive reversion to standard MBA, theories frameworks and concepts often leads to very flawed decisions ( in a good session an amazing large number of people change their initial decision), and C) In fact using the framework is itself part of the problem. Continue reading →

I started my class last Saturday with words of hope that my students’ friends and family were safe. Since I teach in Madison Wisconsin, it was a fair bet that they were not heavily touched. This first response is probably a good starting point. However, where does the discussion in a strategy class go then? Here are a few brief thoughts:

Responding to the humanitarian crisis. From there, one might explore how firms can respond to the humanitarian crisis. Do the Syrian refugees and terror victims all over the world pose an imperative to which businesses must respond? How can they help? What types of businesses can make a real difference?

Responsibility to shareholders. Should firms help even if this hurts shareholder returns? Of course, helping people can build a firm’s reputation. When would this come into play and how can firms position such actions to help firm performance (eliminating any conflict with shareholders)? If it does hurt profitability, when is that justifiable? When is it an imperative?

Global strategy. How should firms develop and execute international strategies in a more uncertain business environment? How should they balance this type of risk in their portfolio?

Employee Welfare. What steps should be taken to assure employee welfare and/or help employees in need?

Opportunity. Some firms may see economic opportunities amid the uncertainty. Of course, defense contractors and security-related firms may win. What other types of firms might see opportunity? See, for example, the video below about Ikea’s refugee shelters or bulletproof blankets for kids in response to school shootings.

Exploitation & Fraud. One of my students pointed out that some firms may take advantage the situation and play off of people’s fears. This might be considered the unethical side of opportunity and is certainly important to discuss as well.

Broader economic impact. Andrew Ross Sorkin offers a brief discussion of this. Conventional wisdom (from studies of the economic impact) is that attacks cause only small blips in GDP and stock markets. However, the political impact and the diversion of resources to agencies like homeland security and defense contractors show up positively in GDP and so understate the impact. Isolationism also may impact global trade well beyond the initial shock.

You may notice that I offer questions rather than answers. I think this topic is fruitful for class discussion and I would hope to learn from the students. I only wish I had answers…

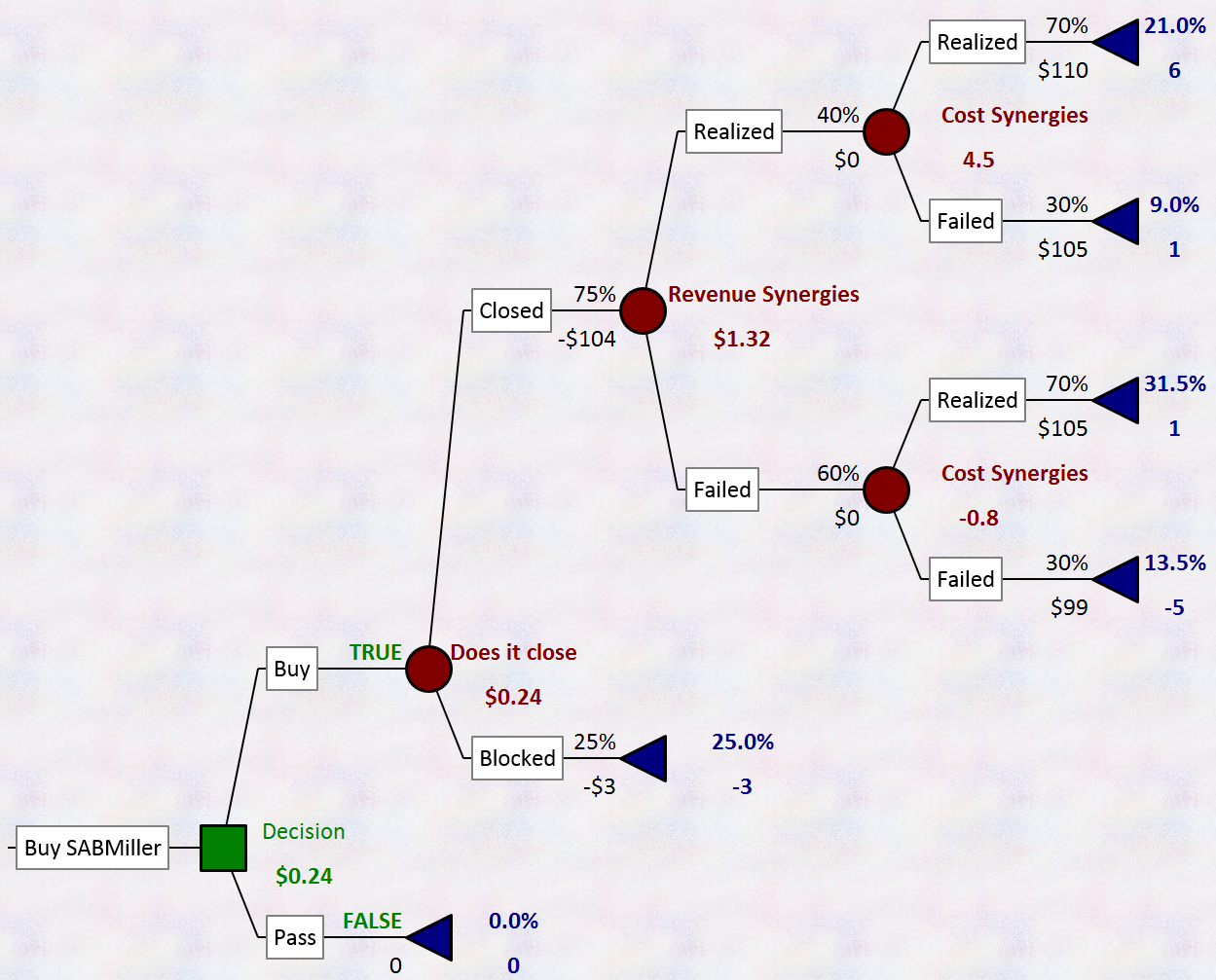

The $104B merger between AB InBev and SABMiller makes a great holiday addition to your classroom. While it is largely a corporate strategy question, I used this discussion to kick off my course and I plan to come back to it as we hit various topics. Here is a packet of news articles that I used as the basis of the case. I also had students complete a brief online poll in advance of the class. This allowed me to start by summarizing their positions and to call on people who I knew had relatively unusual opinions. I used the case to show them how to draw a decision tree (click the image to enlarge) reflecting the uncertainty associated with the acquisition. Of course, it also frames topics throughout the course. Here are a few examples:

Internal capabilities. AB InBev’s capability to conduct acquisitions and to cut costs.

External analysis. Market structure for beer in different countries (namely Africa and China which drive this deal). Also, we compared the market structure for micro- and macro-brews. Of course, these mega-brews act to control distribution channels so barriers to entry are a key part of the game.

Competitive dynamics. Of course this is a game among the rivals but it also includes adjacent industries (like spirits).

Corporate. What are the logics for value creation? For example, to what extent does scale lower manufacturing costs as opposed to purchasing power or other mechanisms. At what point is a larger scale no longer an advantage?

Strategic factor markets: The M&A context makes it clear that most of the synergies go to the target (especially at the 50% bid premium).

Global. As indicated above, this is mostly about entry into new markets (China and Africa, among others).

The NYT Deal Professor notes: “J. Crew, Michelle Obama’s sometime clothing retailer, is yet another struggling private equity buyout. J. Crew’s owners, TPG Capital and Leonard Green & Partners, are stuck, tied to the bargain they struck with the company’s chief executive, Millard S. Drexler. Call it the ‘great man’ problem.” In other words, is the strategic asset a single individual or a set of organizational routines that are robust to key individuals leaving? In this case, J. Crew investors and the board were bound to go with CEO Millard S. Drexler’s recommendations and take the company private. Current struggles suggest limitations to this great man’s capabilities. Indeed, in Leonard Barton’s terms, he is looking more like a core rigidity. This has become a recurring theme. We have explored (in the toolbox) the implications of this for Steve Jobs at Apple but more recently for Jony Ive as Apple’s product development guru. This mini-case may encourage a discussion of strategic human capital, capabilities, organizational routines, and how these relate to corporate governance. Do such key individuals reduce or enhance sustained competitive advantage? Then, along the lines of my own work (Coff, 1999), there is the question of implications for rent appropriation. Clearly Drexler has done well on that front…

Rather than fully embed superior design capabilities in organizational routines, Apple has instead identified and promoted Jony Ive into the design guru role once occupied by Steve Jobs. Ive “worked closely with the late co-founder Steve Jobs, who called Mr Ive his spiritual partner on products stretching back to the iMac.” As before, the reliance on a single person in this role raises key questions: An article published in the New Yorker earlier this year described how “Mr Ive had been describing himself as both ‘deeply, deeply tired‘ and ‘always anxious’ and said he was uncomfortable knowing that ‘a hundred thousand Apple employees rely on his decision-making – his taste – and that a sudden announcement of his retirement would ambush Apple shareholders.‘” Can this be described as an organizational capability? An organizational routine? A dynamic capability? Does it matter that the capability is largely embedded in a single person who is not an owner? All good questions to kick off a nice class discussion…

Contributed by Russ Coff

As evidenced by the business combination scavenger hunt exercise, corporate strategy is always a slippery slope.eBay is in the process of splitting into 3 parts: auctions, Paypal, and the enterprise unit that helps brick and mortar retailers gain an online presence. Their conclusion: these businesses don’t fit together well and are worth more apart than together. Here is a back of the napkin sum of the parts valuation to back that up. This may be a tired story but it won’t go away. In this case, there is no compelling reason that Paypal must be integrated with eBay to be used as a payment mode in auctions. In fact, other marketplaces (like Amazon) may consider Paypal to be a rival instead of a potential partner because it is tied to eBay — more business opportunities if they are separate businesses. Of course, eBay shouldn’t be surprised that an auction would allow one to capture the most value. This might be a nice starting point for corporate strategy. Why do firms have so much trouble determining what combinations will create value?

David Kryscynski (Dr. K) has provided an excellent series of online videos to supplement your course or to help move portions of it online. These are very well produced and may allow you to spend class time on more experiential activities found elsewhere on this site. Below is the video on Porter’s generic strategies but I have provided links to all of the available videos below and listed others that you can gain access to through Wiley. Dr. K’s newest collection can be found on his free web page at LearnStrategy.org.

The videos below are also available but are designed to accompany the textbook: Strategic Management 1e by Jeff Dyer, Paul Godfrey, Robert Jensen and David Bryce (BYU Marriott School of Business). Contact your local Wiley sales representative or Executive Editor, Lise Johnson, at lise.johnson@wiley.com to receive additional information about class-testing or possibly using the videos without the text. For information on how to utilize these animations for non-academic use please send an email to ols_dept@byu.edu.

Much has been made of glass ceilings in organizations and this is a very appropriate conversation for strategy courses. Recent research indicates that appointments of female executives have positive implications for innovation but investor reactions are sometimes negative when such appointments are announced. This video might start the discussion and the research takes it in a more serious direction (as the title suggests, the content may be a bit edgy for some…).

The MicroTech negotiation is a slightly simpler version of another exercise in the Toolbox. It focuses on the problems promoting cooperation across divisions (for example to achieve synergies). MicroTech is a negotiation over the terms to transfer a technology between 2 divisions of a company to take advantage of a market opportunity. Sub-optimal agreements (money left on the table) represent transaction costs and inefficiencies that must be overcome in order to create corporate value. There are two roles (Gant and Coleman). One division, Household Appliances (HA), has developed a new technology that has value if sold outside of the company. However, the division does not have a charter to sell chips. In order to take advantage, the technology must be transferred to the Chips & components (CC) division. In the process, about 20-40% of the potential value is typically left on the table. The discussion focuses on how to align objectives and achieve cooperation across divisions. It turns out that such cooperation is hard to achieve in a competitive culture. How, then, can the firm create a cooperative culture? This, it turns out, may be a VRIO resource…

Rich Makadok invites his students to send pictures of strange business combinations. The sequence of Delta Dental commercials offer humorous combinations of businesses that drive home the topic of corporate strategy. However, these pale when compared to many real world combinations. One of my favorites is when the CEO of Occidental Petroleum (Armand Hammer) purchased a significant interest in the company that makes Arm & Hammer Baking Soda because he liked the name. The scavenger hunt exercise involves asking students to search for real life examples of strange business combinations and bring pictures to class. Once you are looking for them, you realize the examples are everywhere. For example, Boeing plans to produce a new smartphone (really, not a joke). The restaurant above offers family planning advice and products. The exercise will help students realize how rare a sound corporate strategy really is. Click <Continue Reading> to see additional examples (in many cases, you can click the picture to go to the company’s web page):

Few things are more dramatic than a good hostile takeover attempt. Dollar General has been trying all summer to break up the planned nuptials between Family Dollar and Dollar Tree. They have offered $600 million more for Family Dollar than the preferred suitor. Two things may be preventing Family Dollar from switching partners: 1) concerns that a Dollar General deal would be thwarted by anti-trust regulators, and 2) the Family Dollar CEO would lose his job if Dollar General takes over. Of course, they say the second issue is not on their minds. This makes a great “ripped from the headlines” case (here is a small packet of news articles). There are many directions that the discussion can go which, I think, makes for a nice introductory case to frame the rest of the semester. Here are a few:

What is an industry? The anti-trust argument assumes that the industry is defined as small discount stores (in other words, Wal-Mart is not really a player).

Corporate governance: How much should it matter what the Family Dollar CEO’s preferences are?

Cost advantages: Do any of the players have a cost advantage? At what point do the advantages of scale diminish?

Industry structure: What, if anything, makes this an attractive industry?

Competitive dynamics: What will be the next competitive move? What has driven the past moves?

M&A Synergies: The news packet includes an estimate of the synergies and suggests that Dollar General could create more value. Do you buy this analysis?

Is it good business to do good? This is an inevitable question in business strategy. Consider the contrast with economics where the assumption is that societal welfare is maximized when there is perfect competition. In this frame, competitive advantage may imply that societal welfare is sacrificed. Clearly there are examples of firms that have created value for shareholders while destroying it for other stakeholders. This discussion pushes us to consider the question of value creation … for whom? This video includes guest appearances by Jay Barney, Rajshree Agarwal, Jeff McMullen, and Peter Klein.

Often times students become quite disinterested when the topic of agency theory comes up, and they may not completely understand its implications. This short video does a nice job of presenting it in an interesting way in which the students can identify. The context is the relationship between a manager and his assistant, but the discussion can easily be extended to CEOs and the board of directors. Here is another video along similar lines.

CEO pay is back in the news. Harvard Economics professor Greg Mankiw offers a NYT piece on executive compensation and income distributionsuggesting that the public is ok with large incomes of sports stars or actors (like Robert Downey Jr in Iron Man) because they understand how these people contribute. In contrast, understanding what executives add is much more complex. Paul Krugman responds, with an angry rant arguing that few of the top earners are stars or athletes and maintaining his position that executives are greedy and overpaid. This seems like a nice point to debate in a strategy classroom. Are executives overpaid? You might want to conclude the discussion with Alison Mackey’s SMJ article that applies actual data analysis to the question (instead of angry rhetoric). She found that “in certain settings the ‘CEO effect’ on corporate-parent performance is substantially more important than that of industry and firm effects, but only moderately more important than industry and firm effects on business-segment performance.” That is, in some cases, up to 29% of the variance in firm performance can be attributed to the CEO. In the case of a Fortune 500 firm, that could easily amount to billions.

Zappos is moving to a holacracy whereby managers and job titles go by the wayside (see this CNET article among others). This is a real kick in the head to bureaucracy and hierarchy. How does this organizational design mesh with their strategy of customer service and innovation? Another nice example is Valve — see the Valve post on this site. These examples can seed a discussion of strategy, structure, and organizational design as well as a critical analysis of many practices taught in business schools. Such radical forms can be very hard to design and implement. One problem that Foss explores in a recent Organization Science paper is incentives, motivation, and the tendency of managers to meddle in tasks that they say they have delegated. Here is an entertaining Zappo’s commercial to ease into the topic (though one of the many Dilbert videos would be quite compatible as well).

It’s been a red letter week in terms of the

It’s been a red letter week in terms of the

Why isn’t the BCG matrix dead as a framework? I still consistently find that my students have been exposed to it (generally in Marketing). They don’t even understand that it is a framework for internal capital markets (where firms add value by serving as a source of funding) or that it is hopelessly flawed. It’s a dog, divest right away. If the sale generates cash, funnel it to any other management framework (even SWOT) and I’m sure it will create value.

Why isn’t the BCG matrix dead as a framework? I still consistently find that my students have been exposed to it (generally in Marketing). They don’t even understand that it is a framework for internal capital markets (where firms add value by serving as a source of funding) or that it is hopelessly flawed. It’s a dog, divest right away. If the sale generates cash, funnel it to any other management framework (even SWOT) and I’m sure it will create value. What follows is a brief description/outline of the lecture. While it certainly won’t do it justice, it may offer some important ideas for instructors to explore.

What follows is a brief description/outline of the lecture. While it certainly won’t do it justice, it may offer some important ideas for instructors to explore.

another struggling

another struggling  Ive “worked closely with the late co-founder Steve Jobs, who called Mr Ive his spiritual partner on products stretching back to the iMac.” As before, the reliance on a single person in this role raises key questions: An article published in the New Yorker earlier this year described how “Mr Ive had been describing himself as both ‘deeply, deeply tired‘ and ‘always anxious’ and said he was uncomfortable knowing that ‘a hundred thousand Apple employees rely on his decision-making – his taste – and that a sudden announcement of his retirement would ambush Apple shareholders.‘” Can this be described as an organizational capability? An organizational routine? A dynamic capability? Does it matter that the capability is largely embedded in a single person who is not an owner? All good questions to kick off a nice class discussion…

Ive “worked closely with the late co-founder Steve Jobs, who called Mr Ive his spiritual partner on products stretching back to the iMac.” As before, the reliance on a single person in this role raises key questions: An article published in the New Yorker earlier this year described how “Mr Ive had been describing himself as both ‘deeply, deeply tired‘ and ‘always anxious’ and said he was uncomfortable knowing that ‘a hundred thousand Apple employees rely on his decision-making – his taste – and that a sudden announcement of his retirement would ambush Apple shareholders.‘” Can this be described as an organizational capability? An organizational routine? A dynamic capability? Does it matter that the capability is largely embedded in a single person who is not an owner? All good questions to kick off a nice class discussion…

MicroTech is a negotiation over the terms to transfer a technology between 2 divisions of a company to take advantage of a market opportunity. Sub-optimal agreements (money left on the table) represent transaction costs and inefficiencies that must be overcome in order to create corporate value. There are two roles (Gant and Coleman). One division, Household Appliances (HA), has developed a new technology that has value if sold outside of the company. However, the division does not have a charter to sell chips. In order to take advantage, the technology must be transferred to the Chips & components (CC) division. In the process, about 20-40% of the potential value is typically left on the table. The discussion focuses on how to align objectives and achieve cooperation across divisions. It turns out that such cooperation is hard to achieve in a competitive culture. How, then, can the firm create a cooperative culture? This, it turns out, may be a VRIO resource…

MicroTech is a negotiation over the terms to transfer a technology between 2 divisions of a company to take advantage of a market opportunity. Sub-optimal agreements (money left on the table) represent transaction costs and inefficiencies that must be overcome in order to create corporate value. There are two roles (Gant and Coleman). One division, Household Appliances (HA), has developed a new technology that has value if sold outside of the company. However, the division does not have a charter to sell chips. In order to take advantage, the technology must be transferred to the Chips & components (CC) division. In the process, about 20-40% of the potential value is typically left on the table. The discussion focuses on how to align objectives and achieve cooperation across divisions. It turns out that such cooperation is hard to achieve in a competitive culture. How, then, can the firm create a cooperative culture? This, it turns out, may be a VRIO resource…

They have offered $600 million more for Family Dollar than the preferred suitor. Two things may be preventing Family Dollar from switching partners: 1) concerns that a Dollar General deal would be thwarted by anti-trust regulators, and 2) the Family Dollar CEO would lose his job if Dollar General takes over. Of course, they say the second issue is not on their minds. This makes a great “ripped from the headlines” case (

They have offered $600 million more for Family Dollar than the preferred suitor. Two things may be preventing Family Dollar from switching partners: 1) concerns that a Dollar General deal would be thwarted by anti-trust regulators, and 2) the Family Dollar CEO would lose his job if Dollar General takes over. Of course, they say the second issue is not on their minds. This makes a great “ripped from the headlines” case ( suggesting that the public is ok with large incomes of sports stars or actors (like Robert Downey Jr in Iron Man) because they understand how these people contribute. In contrast, understanding what executives add is much more complex.

suggesting that the public is ok with large incomes of sports stars or actors (like Robert Downey Jr in Iron Man) because they understand how these people contribute. In contrast, understanding what executives add is much more complex.